In the fast-paced and ever-evolving landscape of the logistics and trucking industry, securing financing is paramount for success and sustainability. As trucking businesses continually face rising operational costs, fluctuating fuel prices, and stringent regulatory requirements, access to reliable funding becomes critical in maintaining competitive advantage. The ability to finance acquisitions, manage cash flow, and invest in technology can be the deciding factor between thriving and merely surviving in this market. For small and medium-sized trucking companies, the challenges are even more pronounced. Many lack the necessary capital for expansions, often grappling with delayed payments from clients that can hinder everyday operations. According to a recent report from the American Trucking Associations, the financing gap in trucking is estimated at $600 billion annually, underscoring the urgency for tailored financial solutions such as freight factoring and equipment leasing. This financing landscape has further evolved, offering innovative methods for securing necessary funds without the burden of traditional loans, which often require extensive credit history and collateral. As the industry adapts to the post-pandemic economic recovery and the rising demands for efficiency and reliability, understanding how to navigate the complexities of truck financing is essential. This article aims to unravel the options available for trucking businesses seeking loans, providing insights into effective strategies and solutions tailored to your unique needs. By exploring various financing avenues, including modern methodologies designed specifically for the trucking sector, we will help you equip your business to not only meet current challenges but also seize growth opportunities effectively.

Types of Trucking Business Loans Available

When seeking financing for a trucking business, operators can consider various loan options that cater specifically to their requirements. Understanding the distinctions between Traditional Bank Loans, Equipment Financing, and Government-Backed Loans is crucial for making an informed decision that aligns with business needs.

1. Traditional Bank Loans

Overview

Traditional bank loans have long served as a primary funding source for many trucking companies. These loans are typically characterized by fixed interest rates, longer repayment terms, and stable funding.

Pros

- Predictable Interest Rates: Traditional banks usually offer fixed rates, allowing businesses to estimate their monthly payments over time.

- Long Repayment Terms: Borrowers can benefit from extended payment periods, often maximizing cash flow management for large purchases.

- Established Relationships: Companies that have a history with banks may enjoy easier access to capital through personal or business connections.

Cons

- Stricter Qualification Criteria: In 2023, many banks tightened lending standards, requiring strong credit scores (700+) and significant collateral. It can be challenging for smaller operators to qualify.

- Lengthy Approval Process: The process can take 4 to 6 weeks, delaying fleet expansion and finances when time-sensitive opportunities arise.

- High Documentation Requirements: Extensive paperwork can be a burden, particularly for newer businesses without adequate financial records.

For a more detailed assessment of the challenges in securing traditional bank loans, you can explore this study from the Federal Reserve.

2. Equipment Financing

Overview

Equipment financing allows trucking businesses to obtain essential vehicles without making a large upfront payment. This option typically includes the truck or equipment as collateral, reducing the lender’s risk.

Pros

- Preserves Cash Flow: Operators can maintain lower monthly costs compared to purchasing outright.

- Access to Upgraded Equipment: This financing method opens doors for acquiring modern and efficient trucks without the need for large capital at once.

- Tax Benefits: Businesses may take advantage of depreciation deductions for financed equipment, offering potential tax relief.

Cons

- Interest Payments: Interest can add up, leading to increased costs over the life of the loan.

- Risk of Equipment Outlasting Loan Terms: Operators may find themselves locking into a loan that lasts longer than the useful life of the equipment, which can create future financial strain.

- Down Payment Requirements: Typically, a percentage of the loan is required upfront, adding to initial costs.

For insights on balancing ownership costs and financing strategies, consider reading about equipment financing options.

3. Government-Backed Loans

Overview

Government-backed loans, such as those from the Small Business Administration (SBA), aim to help trucking companies access capital that might be hard to secure through traditional means. These loans often come with lower interest rates and more favorable terms.

Pros

- Lower Interest Rates: These loans typically have better rates compared to conventional financing.

- Longer Repayment Terms: Options often extend to 10 years, providing ease in managing cash flow.

- Liberal Eligibility Criteria: Compared to traditional loans, eligibility requirements may be less restrictive, expanding access to smaller operations.

Cons

- Lengthy Application Process: Applications can take weeks, delaying necessary funding.

- Personal Guarantees Required: Owners may need to secure the loan with personal assets, which adds risk.

- Restrictions on Use of Funds: Funds must be used for specific purposes as approved by the SBA, limiting flexibility.

To delve deeper into how these loans work and their impact on truckers, you can visit this guide by the SBA.

Conclusion

Choosing the right type of loan for a trucking business is a critical decision that can impact its long-term success. Operators need to weigh the pros and cons of each financing option carefully. Whether opting for a traditional bank loan, equipment financing, or a government-backed loan, understanding each route’s implications will empower businesses to make informed financial decisions.

An infographic summarizing types of trucking business loans and their respective pros and cons.

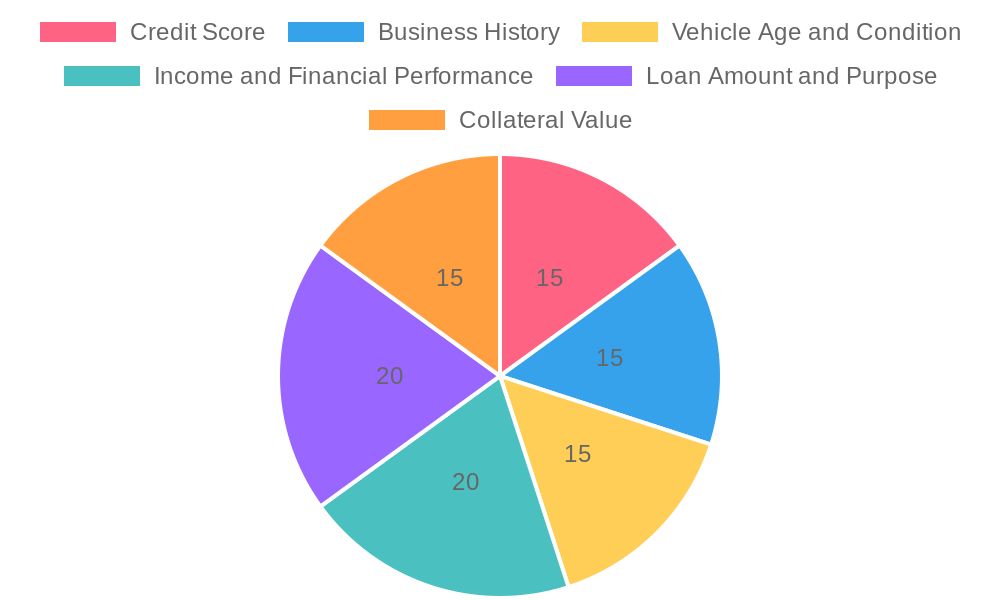

Key Factors Lenders Consider When Approving Trucking Business Loans

When seeking financing for your trucking business, understanding the criteria that lenders evaluate can significantly enhance your chances of approval. Here are the critical factors that play a vital role in the loan application process:

-

Credit Score and History

A solid credit profile is fundamental. Lenders commonly assess both personal and business credit scores. A higher score often translates to better interest rates and terms. Additionally, they review the applicant’s credit history, including repayment patterns and outstanding debts. -

Business Age and Stability

Lenders typically prefer established businesses with a proven track record. A company that has been operational for at least one year usually has a better chance, as it demonstrates stability and experience in the industry. -

Vehicle Condition and Age

The age and condition of the trucks being financed are crucial. Newer, well-maintained vehicles are perceived as lower risk. Lenders often require maintenance records and depreciation assessments to gauge asset value over time. -

Income and Financial Performance

Lenders look at the business’s revenue trends and profitability. Consistent income streams reflect operational reliability. Tracking average monthly income for 12-24 months helps establish revenue stability, which is a key consideration in the approval process. -

Debt-to-Income Ratio (DTI)

This ratio measures total monthly debt payments against gross monthly income. A DTI of below 35-40% is typically viewed favorably by lenders, as it indicates that the business can comfortably manage its debt obligations. -

Cash Flow Analysis

A positive cash flow is essential for loan approval. This includes examining the average time to collect payments (days receivable) and ensuring there are sufficient reserves to cover unforeseen expenses. -

Collateral Value

If the loan is secured, the value of the collateral (e.g., trucks or equipment) is critically evaluated. Lenders will often assess whether the collateral can adequately cover the loan amount should repayment issues arise. -

Industry Experience

Lenders favor businesses led by experienced individuals who understand the complexities of the trucking industry. A proven safety record and operational efficiency can bolster an application significantly. -

Clear Business Plan

A well-defined business plan that outlines how the funds will be utilized (e.g., for fleet expansion, equipment upgrades, or working capital) enhances credibility. Additionally, demonstrating realistic financial projections and a sensible repayment schedule is crucial.

Visual Representation of Loan Approval Factors

Detailed Metrics for Trucking Loan Approval

A comprehensive overview of key financial and operational metrics that lenders typically evaluate includes:

| Criteria | Key Financial and Operational Metrics |

|---|---|

| Creditworthiness | – Personal and business credit scores – Debt repayment history – Credit utilization ratio |

| Revenue Stability & Volume | – Average monthly revenue (12-24 months) – Consistent freight volume – Revenue growth trend (YoY) |

| Profitability | – Net profit margin (after expenses) – EBITDA metrics – Owner’s draw vs. net income |

| Debt-to-Income Ratio (DTI) | – Monthly debt payments vs. gross monthly income – Ideally below 35-40% |

| Cash Flow Management | – Monthly cash flow – Days receivable (collection period) – Cash reserves for expenses |

| Truck & Asset Health | – Age and maintenance of trucks – Asset value assessments – Availability of backups |

| Industry Experience & Track Record | -Years in the industry – Number of drivers – Safety record compliances |

| Business Plan & Use of Funds | – Purpose for the loan – ROI projections – Cash flow alignment with repayment schedule |

Understanding these factors can not only help you prepare your application more effectively but also aid in enhancing your business’s overall financial health. For more specific insights into the trucking industry and the challenges faced, learn more about industry economics.

Improving Loan Approval Chances for Trucking Businesses

Securing a loan is essential for trucking businesses looking to grow or sustain operations, whether for purchasing new equipment, expanding their fleet, or managing day-to-day expenses. However, the process of gaining approval can be challenging. To navigate through the complexities of loan approval, here are key expert insights and strategies to enhance your chances of securing financing.

Understanding the Key Elements of Loan Approval

1. Maintain a Strong Credit Score

A solid credit score is critical. Lenders typically prefer a personal credit score of at least 700 and a business credit score above 150 (Dun & Bradstreet). This indicates your reliability to meet financial commitments. Regularly check your credit report for errors and pay off debts to improve your score over time.

2. Prepare Detailed Financial Statements

Lenders require comprehensive financial statements for at least the last two to three years. This includes profit and loss statements, balance sheets, and cash flow statements. Accurate, consistent figures in these documents demonstrate financial stability. According to Bankrate, strong financial management plays a crucial role in loan approval.

3. Develop a Comprehensive Business Plan

Having a well-thought-out business plan is essential. This should include:

- Market analysis

- Operational strategies

- Fleet expansion plans

- Revenue projections

This information not only shows lenders that you are prepared but also demonstrates how you intend to generate revenue and manage cash flow effectively. The SBA emphasizes the importance of a solid business plan in securing loans.

Financial Management and Cash Flow

4. Manage Cash Flow Effectively

Demonstrating a history of timely payments and managing cash flow can significantly influence your loan approval. Lenders look for predictable income streams, so keeping detailed records of fuel expenses, maintenance costs, and freight invoices is vital. Employ tools like QuickBooks or Xero to provide liquidity reports and demonstrate financial health.

5. Choose the Right Lender

Selecting a lender who specializes in trucking loans can streamline the approval process. Companies like TransAmerica and FleetCor understand the specific needs and challenges of the trucking industry, which can lead to more favorable terms and conditions.

Characteristics Lenders Look For

6. Provide Collateral or Asset Documentation

Offering collateral, such as vehicle titles or equipment leases, can enhance your loan application. Clearly document ownership and appraised values of these assets, as it reassures lenders about the security of their investment.

7. Minimize Debt-to-Income Ratio

Keep your existing debt low relative to your income. Aim to maintain a debt ratio below 35%. Reducing personal or business liabilities before applying can result in better loan terms.

8. Apply With a Complete Application Package

Submit a complete application package that includes all pertinent documents:

- Business licenses

- Tax returns

- Driver qualifications

- Insurance certificates

Thorough preparedness can speed up the approval process and prevent delays due to missing documentation.

Additional Strategies for Success

9. Consider a Co-Signer or Guarantor

If your creditworthiness is not optimal, having a co-signer with excellent credit can significantly boost your chances of approval. Lenders view this as a risk mitigation strategy, thereby increasing their confidence in lending.

10. Follow Up and Build Relationships

Establishing a personal relationship with your lender can open doors to better communication and flexibility in lending terms. Following up on your application status can also show your commitment and seriousness in securing the financing.

Conclusion

In conclusion, understanding the nuances of loan applications within the trucking industry can provide you with a competitive edge. By following these strategies-maintaining strong credit, preparing detailed financial documentation, and choosing the right lenders-you can significantly increase your chances of loan approval, allowing your business to thrive in a competitive marketplace.

For more information, refer to Bank of America for comprehensive loan options tailored to trucking businesses.

Comparative Table of Trucking Business Loan Providers

Here’s a detailed comparison of various loan providers specialized in trucking businesses, focusing on interest rates, terms, and application requirements:

| Loan Provider | Interest Rates | Loan Terms | Application Requirements |

|---|---|---|---|

| Capixa | Customized rates based on creditworthiness | Flexible, tailored for trucking | Business profile, credit history, equipment purchase details |

| Bankrate | 6% – 35%+ | Depends on the type of truck being financed | Minimum credit score 650+, proof of income, stability in business (2+ years) |

| U.S. News & World Report | 6% – 15% (Equipment Loans) | Various options available | Minimum credit score (often 650+), stable business history (2+ years), proof of income |

For more information on how trucking loans work, check out U.S. News for detailed resources.

Alternatively, for tailored business solutions, explore Capixa’s offerings.

Preparing to Apply for a Trucking Business Loan

Navigating the process of securing a trucking business loan can be complex, especially for logistics companies, construction firms, fleet management enterprises, or food and beverage distributors. Being well-prepared can make a substantial difference in the outcome of your loan application. Here are the essential steps prospective borrowers should take to prepare effectively.

1. Understand Your Business Needs

Before applying for a loan, it is vital to determine exactly how much funding you need and for what purpose. Consider the following:

- Identify Specific Financial Needs: Determine whether you need funds for purchasing trucks, expanding your fleet, investing in technology, or improving operational facilities.

- Estimate Costs: Create a detailed estimate of costs related to your intended investment, including vehicle costs, insurance, operating expenses, and any potential unexpected costs.

2. Gather Necessary Documentation

Having the right documents in order is critical to streamline your application process. Essential documentation includes:

| Document | Description |

|---|---|

| Business Plan | Detailed outline of how the loan will benefit your business, including financial projections and strategic plans. |

| Financial Statements | Recent business and personal financial statements to assess cash flow and earnings. |

| Tax Returns | Business and personal tax returns for the last 2-3 years. |

| Credit Report | A report detailing your credit history and score; examine it for accuracy. |

| Vehicle Ownership Proof | Documentation showing ownership of existing vehicles or lease agreements for trucks. |

| Operating Licenses | Current Department of Transportation (DOT) and Motor Carrier (MC) numbers. |

| Loan Purpose Letter | A letter describing the purpose of the loan and how it will be repaid. |

Gathering these documents ensures that you present a clear and comprehensive picture of your business’s financial health and how the loan fits into your overall business strategy. For a more detailed list of required documentation, you can refer to resources from the U.S. Small Business Administration.

3. Improve Your Credit Score

A strong credit score is often critical in securing favorable loan terms. To improve your creditworthiness:

- Make Timely Payments: Pay all bills promptly, as payment history is a key factor in credit scoring. According to Experian, your payment history accounts for 35% of your FICO score.

- Reduce Credit Utilization: Aim to keep your credit utilization ratio below 30%. This term refers to the amount of credit you use compared to your total available credit.

- Limit New Credit Applications: Avoid applying for new credit accounts within six months of applying for a loan, as hard inquiries can negatively affect your score.

- Dispute Errors: Regularly check your credit report for inaccuracies and dispute any errors that may exist, as they can unfairly impact your score.

- Maintain Old Accounts: Keeping older credit accounts open can lengthen your credit history, which benefits your score.

By consistently managing these practices, you can improve your overall credit profile and increase your chances of loan approval.

4. Create a Solid Business Plan

Having a well-thought-out business plan is not just for your loan application; it also serves as a guideline for your business. Here’s what to include:

- Executive Summary: Briefly describe your business, its goals, and how the loan will help to fulfill those goals.

- Market Analysis: Conduct research on the trucking industry, recognizing competitors, and target markets you wish to serve.

- Financial Projections: Include projected revenue, profit margins, and a break-even analysis to demonstrate how you plan to repay the loan.

- Operational Strategy: Describe how you plan to run your business effectively and efficiently.

5. Consult with Professionals

Engaging with financial advisors or accountants who understand the trucking industry can be incredibly beneficial in preparing your financing strategy. They can help refine your business plan, evaluate financial risks, and suggest practical financial practices to enhance your loan application.

6. Apply for the Loan

Once you have gathered all the necessary documentation and completed your business plan:

- Choose the Right Lender: Research lenders who specialize in trucking loans and compare interest rates, loan terms, and requirements.

- Submit Your Application: Ensure that your application is complete, accurate, and submitted on time. Provide any supplementary documents requested by the lender to enhance your application.

Conclusion

Preparing to apply for a trucking business loan involves several proactive steps-understanding your needs, gathering essential documentation, improving your credit score, and creating a robust business plan. A methodical approach will not only enhance your chances of securing the loan but also set your business on a path to growth and success.

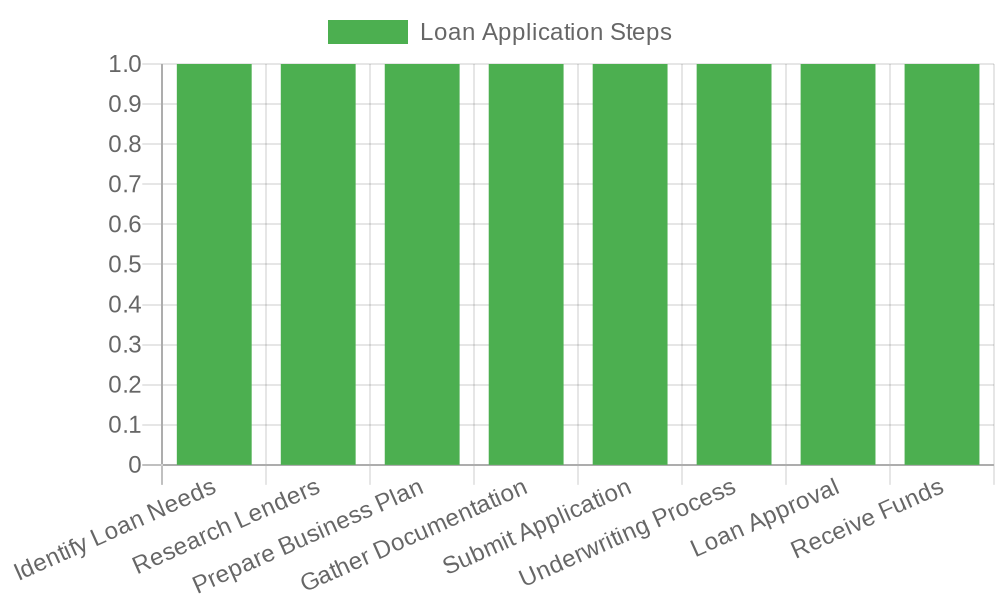

Trucking Business Loan Application Process Flowchart

| Step | Key Actions | Description |

|---|---|---|

| 1. Identify Loan Needs | Determine purpose (e.g., new truck purchase, fleet expansion, working capital) and required amount | Assess financial goals and calculate exact funding needs based on business requirements |

| 2. Research Lenders | Compare lenders specializing in commercial or trucking loans (e.g., banks, credit unions, online lenders) | Evaluate interest rates, terms, fees, eligibility criteria, and customer reviews |

| 3. Prepare Business Plan | Develop a concise plan including company overview, market analysis, revenue projections, and use of funds | Highlight business stability, growth potential, and repayment capacity to build lender confidence |

| 4. Gather Documentation | Collect essential documents: business licenses, tax returns, financial statements, truck titles, insurance, and personal credit history | Ensure all paperwork is complete, accurate, and up-to-date |

| 5. Submit Application | Complete loan application form through lender’s platform or in person | Provide all requested information and supporting documents for review |

| 6. Underwriting Process | Lender evaluates creditworthiness, business performance, collateral value, and risk profile | May include additional verification requests or interviews |

| 7. Loan Approval | Lender issues formal approval with terms (interest rate, repayment schedule, loan amount) | Review and accept offer before finalizing the agreement |

| 8. Receive Funds | Funds are disbursed via direct deposit or check, typically within 1-10 business days after signing | Use funds according to agreed-upon purpose for optimal business impact |

Note: This flowchart is designed for clarity and visual engagement. Actual timelines may vary by lender and individual circumstances.

Sources:

- SBA.gov – Small Business Loans

- Bankrate – Commercial Truck Loan Guide

- NerdWallet – Business Loan Comparison Tools

Importance of Preparation in Securing Trucking Business Loans

When it comes to applying for loans, especially for trucking businesses, careful preparation is crucial. As financing expert John Doe states:

“Instead of waiting for the bank to request items one by one, send a complete, organized package up front: recent financials, projections, and supporting documentation. This demonstrates professionalism and significantly increases your chances of approval.”

This emphasis on proactive preparation highlights how essential it is for logistics and freight companies to be ready when seeking financial support.

For a deeper understanding of navigating the financial landscape, you might want to learn more about economic challenges in the trucking industry.

Conclusion: The Crucial Role of Loans in Trucking Business Growth

In the dynamic landscape of the trucking industry, securing the right loans has become a fundamental aspect of fostering growth and ensuring long-term sustainability. As logistics and freight companies, construction and engineering firms, fleet management companies, and food and beverage distributors navigate an evolving market, having access to crucial funding can make the difference between stagnation and success.

Loans serve as a powerful tool that allows these businesses to invest in essential operational upgrades and equipment necessary for maintaining a competitive edge. From purchasing new vehicles and technology upgrades to facilitating expansions into new markets, the strategic use of loans can drive significant business growth. For instance, companies that effectively manage loan capital can enhance their operational efficiency, thereby reducing overhead costs and improving customer service, leading to increased revenues.

Moreover, as highlighted in recent studies, obtaining commercial truck loans can help companies stabilize their cash flow during challenging economic times. Businesses can use these funds to cover essential expenses, such as payroll and maintenance, ensuring seamless operations without interruption. A well-timed loan can also support companies in scaling operations in response to rising demand, thereby enhancing their market presence and profitability.

Additionally, investments made possible through loans can lead to innovation. As the trucking industry moves towards more sustainable practices, financing options allow businesses to adopt electric or hybrid vehicles and invest in technology that reduces emissions and enhances efficiency. Companies like Coke Canada highlight the benefits of such advancements, showcasing how investment and growth go hand in hand.

Given the complex nature of the trucking industry’s financial landscape, it is imperative for business leaders to approach the loan acquisition process thoughtfully. They must assess their unique needs and carefully evaluate available financing options to ensure that they select products best suited to their strategic goals. Working with experienced financial advisors or loan specialists can provide invaluable insights into navigating the lending process, ultimately securing the best terms to promote stability and growth.

As we look to the future, the trucking industry stands at a crossroads of innovation and demand. Companies that recognize the importance of financing solutions as a cornerstone of their growth strategy will be better positioned to thrive amid competition and shifting consumer preferences. Securing loans not only empowers business expansion but also fosters an environment of resilience, enabling companies to adapt to changing market conditions with agility.

With the right approach and resources, your trucking business can not only survive but flourish. Take action today by exploring your loan options and investing in the future of your operations. Expand your capacity and capability by partnering with the right financial institution to tailor a loan solution designed for your business needs.

Don’t wait for opportunities to come knocking. Secure your trucking business’s future today by understanding and utilizing loan options. For more information on how to leverage financial tools for growth, visit Titan Business Trucks. With the right financial support, your business can not only meet the challenges of today but also seize the opportunities of tomorrow for a prosperous future.